Embedded Supply Chain Finance - 2026 Report

India’s MSME ecosystem forms the backbone of the economy, yet access to timely and affordable working capital remains a persistent challenge. This report explores how Embedded Supply Chain Finance (E-SCF) is transforming MSME credit by integrating financing directly into business workflows.

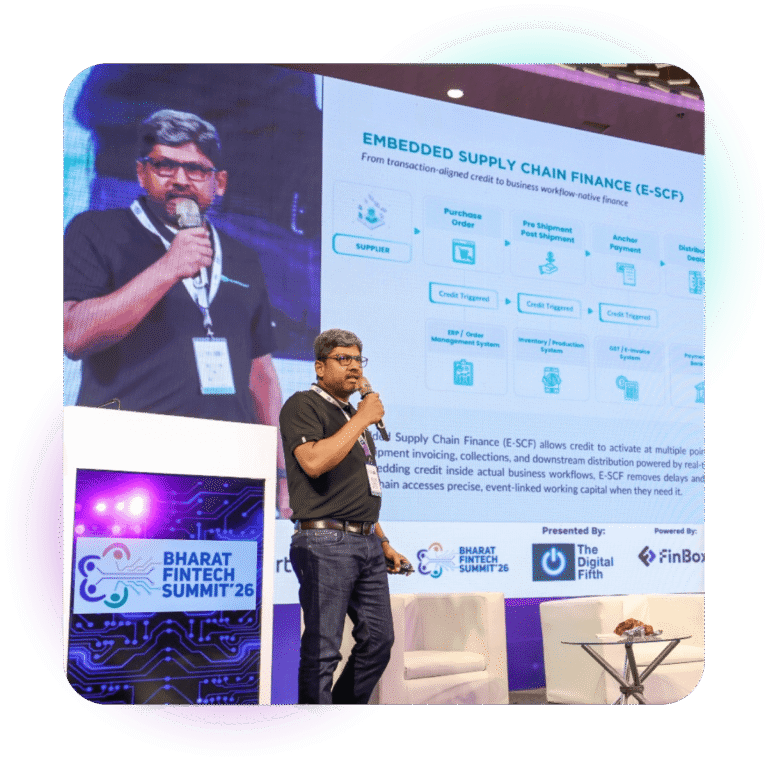

The 2026 “Embedded Supply Chain Finance” report highlights how API-led platforms, real-time data flows, and ecosystem collaboration are enabling a shift from traditional lending models to transaction-driven, workflow-native finance, unlocking scalable and inclusive credit access across supply chains.

Key Trends Transforming Supply Chain Finance

1. Shift from Traditional Lending to Embedded Finance

- Workflow-Native Credit: Financing is no longer accessed separately but embedded within ERP, invoicing, and payment systems.

- Event-Driven Lending: Credit is triggered at key stages like purchase orders, invoicing, and collections, aligning capital with real trade activity.

2. API-Led Infrastructure & Real-Time Integration

- Deep System Integration: Platforms integrate anchor ERPs, MSME systems, and lender APIs to enable seamless credit flows.

- Automated Decisioning: Real-time data enables faster underwriting, instant limit validation, and automated disbursement.

3. Expansion Across the Supply Chain

- Beyond Tier-1 Financing: E-SCF extends credit access to Tier-2/3 suppliers, distributors, and retailers.

- Full Value Chain Coverage: Solutions now span to all the participants from upstream (suppliers) to downstream (dealers and retailers).

4. Product Evolution in SCF

- High-Growth Products: PO financing, invoice discounting, dealer financing, and channel financing are gaining momentum.

- Shift from Traditional Credit: Working capital loans and overdrafts are gradually being complemented by more dynamic, transaction-linked solutions.

5. Data-Driven Risk & Credit Models

- Transaction-Based Underwriting: Credit decisions are increasingly based on verified trade flows rather than static financials.

- Continuous Risk Monitoring: Real-time visibility into orders, inventory, and payments improves risk control and reduces NPAs.

Opportunities & Challenges

Opportunities

- Massive Market Potential: SCF is projected to grow rapidly, reaching ~₹21 lakh crore, driven by rising MSME credit demand.

- Improved Credit Access: Embedded models reduce friction, enabling faster and more affordable financing for underserved MSMEs.

- Operational Efficiency: Automation across onboarding, disbursement, and reconciliation lowers costs and improves scalability.

Challenges

- Integration Complexity: Deep ERP and ecosystem integration requires significant coordination across stakeholders.

- Ecosystem Dependence: Success depends on alignment between anchors, lenders, and platforms, not just individual adoption.

- Data Standardization: Inconsistent data quality and formats can limit scalability and interoperability.

Looking Ahead: The Future of E-SCF in India

- Embedded by Default: Credit will increasingly become invisible fully integrated into business processes rather than accessed separately.

- API-First Ecosystems: Standardized integrations will enable multi-lender, multi-anchor participation at scale.

- Real-Time Credit Infrastructure: Continuous data flows will power dynamic limits, automated settlements, and proactive risk management.

- Deeper MSME Inclusion: Expansion into lower tiers of the supply chain will drive financial inclusion and economic resilience.

Conclusion

Embedded Supply Chain Finance marks a fundamental shift from traditional lending to workflow-integrated, real-time credit aligned with actual trade activity. By leveraging API-led infrastructure, continuous data flows, and ecosystem collaboration, E-SCF enables faster, more accessible, and scalable financing for MSMEs. As India’s financial landscape evolves, the ability to seamlessly embed credit into business processes will be key to driving financial inclusion and unlocking the next phase of MSME growth.